Melinda Jennison – Streamline Property Buyers

Introduction

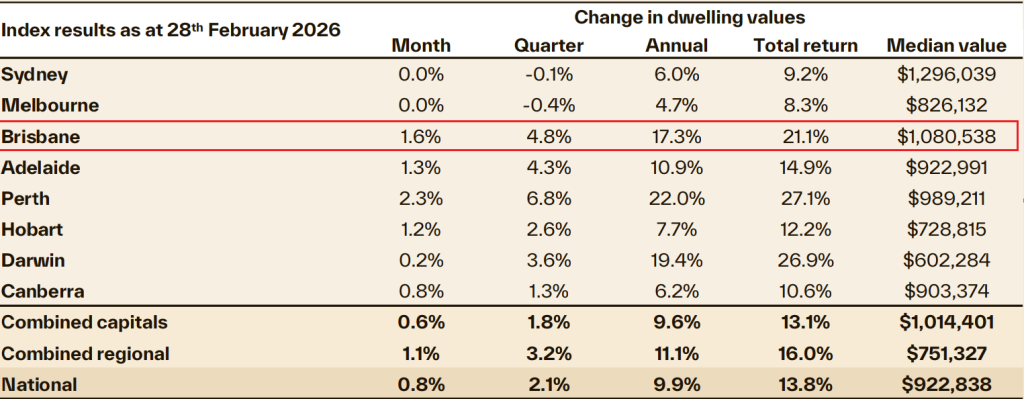

February 2026 has reinforced Brisbane’s position as one of Australia’s strongest performing property markets. According to Cotality’s Home Value Index to 28 February 2026, Brisbane dwelling values rose 1.6% for the month, matching January’s result, with the annual gain accelerating to 17.3%, up from 15.7% in January. The median dwelling value now sits at $1,080,538, compared with $1,054,555 a month prior. On a five-year basis, Brisbane values have risen 86.1%, a testament to the durable structural shift in demand that has unfolded across southeast Queensland in the post-pandemic era. At a time when some markets are stalling, Brisbane continues to demonstrate the kind of consistent monthly momentum that compounds meaningfully over time.

The national picture is increasingly divided. Sydney and Melbourne recorded 0.0% monthly growth, slipping into negative rolling quarterly territory at -0.1% and -0.4% respectively. The divergence between Australia’s two largest markets and the mid-tier capitals is stark. Brisbane (1.6%), Adelaide (1.3%), Hobart (1.2%) and Perth (2.3%) all materially exceeded the combined capitals’ 0.6% monthly result. On an annual basis, only Perth (22.0%) and Darwin (19.4%) surpassed Brisbane’s 17.3% gain, with Sydney (6.8%) and Melbourne (5.5%) lagging considerably. This gap has continued to widen in recent months, with no signs of meaningful convergence on the immediate horizon.

A notable structural shift is also emerging in buyer composition. ABS data shows loans to first-home buyers rose 6.8% from the September to December quarter of 2025, and are 9.1% higher than December 2024, the strongest result in two years, with volumes at their highest level since March 2022.

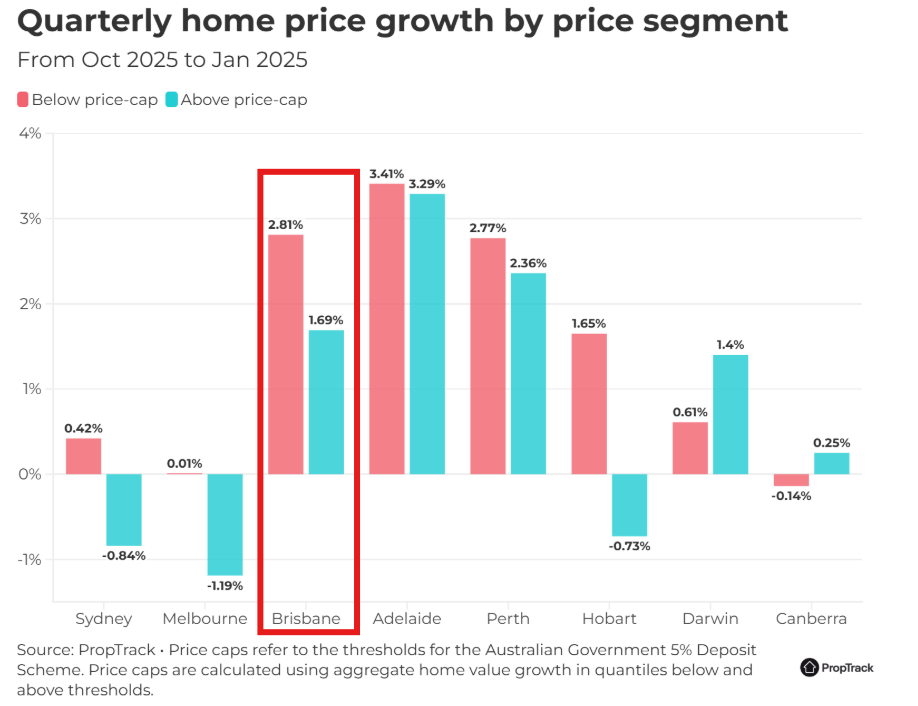

Queensland, NSW, Western Australia and the ACT led state-level gains. The Federal Government’s 5% deposit guarantee and Help to Buy initiative are clearly supporting this cohort, reducing the time required to save a deposit and expanding the range of accessible properties.

This dynamic appears to be influencing price growth across different value segments, with price movements below scheme price caps much stronger than those above, a trend clearly evident in Brisbane’s market segment data.

Supply conditions remain the primary driver of Brisbane’s strength. According to SQM Research, new listings in Brisbane during January were 15.3% lower than a year ago, with total listings down 22.8% year-on-year, one of the largest declines of any capital city. Brisbane’s total listing stock sits 31% below its five-year average. This chronic shortage gives buyers few choices and sellers the upper hand at negotiation.

Auction clearance rates averaged 70.4% through February, significantly above year-ago levels and well above the threshold typically associated with rising prices. Even the February RBA rate hike to 3.85%, the first increase since November 2023, did little to dampen immediate auction momentum, confirming that the supply-demand imbalance currently outweighs the near-term drag from higher borrowing costs.

Brisbane Dwelling Values

Brisbane’s median dwelling value reached $1,080,538 in February, up from $1,054,555 in January. Quarterly growth of 4.8% eased marginally from January’s 5.1%, though the annual result of 17.3% marks a clear acceleration.

Source: Cotality

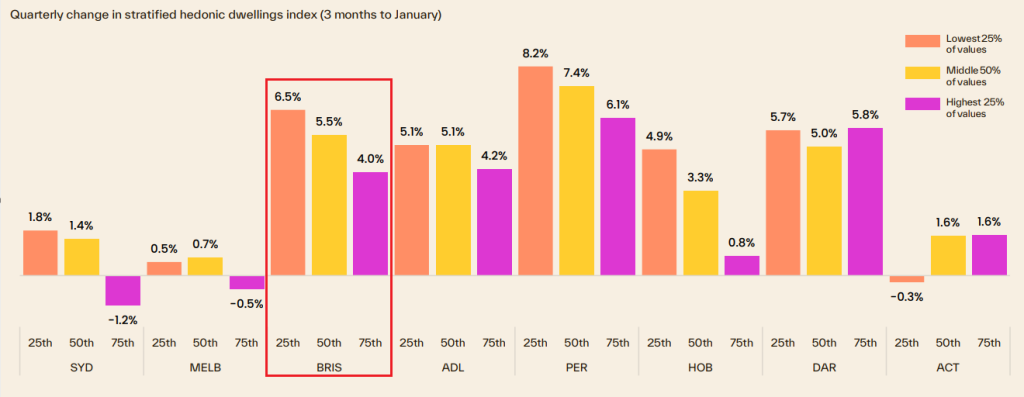

Cotality’s stratified index for the three months to January shows the lowest 25% of dwellings rose 6.5%, the middle 50% gained 5.5%, and the highest 25% rose 4.0%, compared with 6.8%, 5.9% and 4.6% respectively in the prior quarter. While growth has moderated fractionally across all segments, the pattern remains consistent. The lower end of the market continues to outperform, driven by concentrated buyer competition from first-home buyers and investors operating below the $1 million price point.

Source: Cotality

Proptrack confirmed dwelling price growth of 0.7% for February.

Brisbane House Values

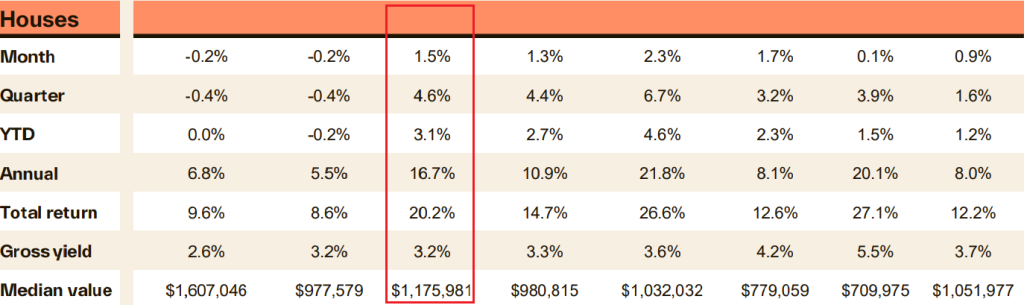

The median house value in Greater Brisbane rose to $1,175,981 in February, up from $1,149,589 in January. Monthly growth of 1.5% was unchanged from the prior month, whilst the quarterly gain eased slightly to 4.6% from 4.9%. The annual result of 16.7% represents a meaningful acceleration from January’s 15.1%, placing Brisbane amongst the national leaders, exceeded only by Perth (21.8%) and Darwin (20.1%).

For context, Sydney’s annual house growth is 6.8% and Melbourne’s 5.5%, highlighting the scale of Brisbane’s outperformance.

Gross yields remain steady at 3.2%, unchanged from last month. Including rental income, the total annual return on a Brisbane house over the past twelve months is estimated at approximately 20.2%, a figure that continues to attract both local and interstate investment.

Proptrack reported house price growth of 0.6% for February, indicating a reacceleration from the prior month.

Source: Cotality

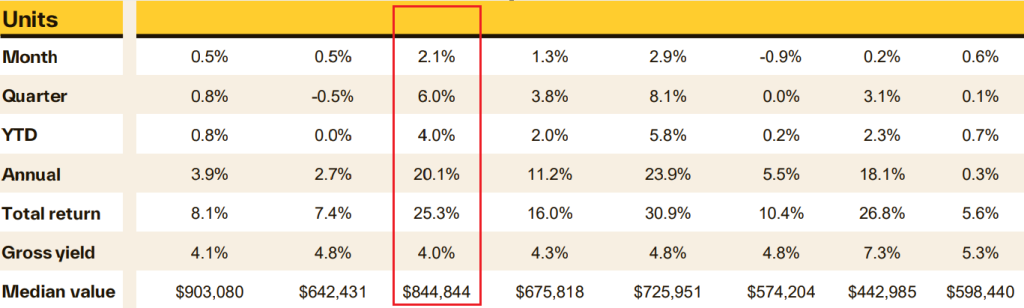

Brisbane Unit Values

Brisbane’s unit market continues to be the standout performer. The median unit value reached $844,844 in February, up from $824,764 in January. Monthly growth of 2.1% edged higher than January’s result, whilst the annual gain of 20.1% marks a reacceleration from 18.3% last month.

The unit market is benefiting from multiple tailwinds, including worsening housing affordability pushing buyers into the attached dwelling segment, continued investor demand attracted by a 4.0% gross yield, and rental market conditions that continue to reward income-focused property holders. Total annual return for Brisbane units, including rental income, is estimated at approximately 25.3%, the second highest of any capital city. Only Perth (23.9%) recorded stronger annual unit growth amongst the capitals.

Proptrack reported unit price growth of 0.9% for February, reaccelerating from the prior month.

Source: Cotality

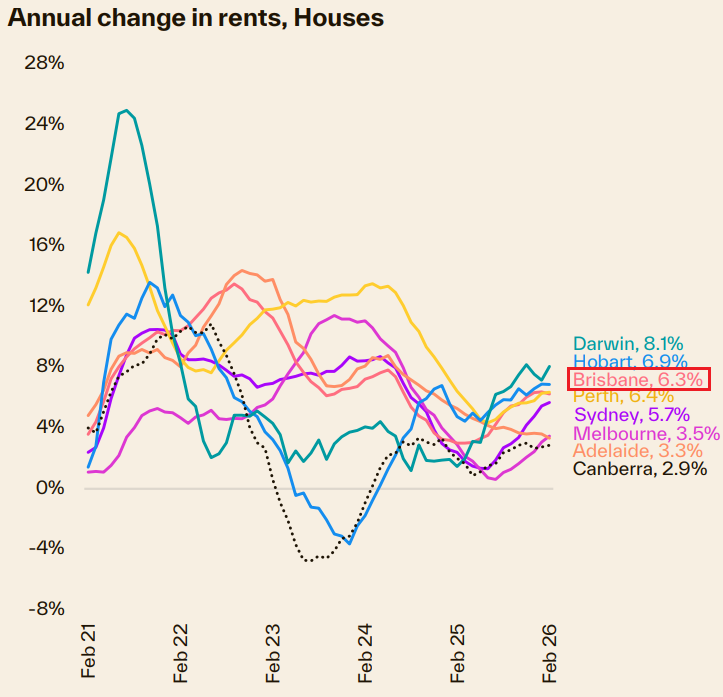

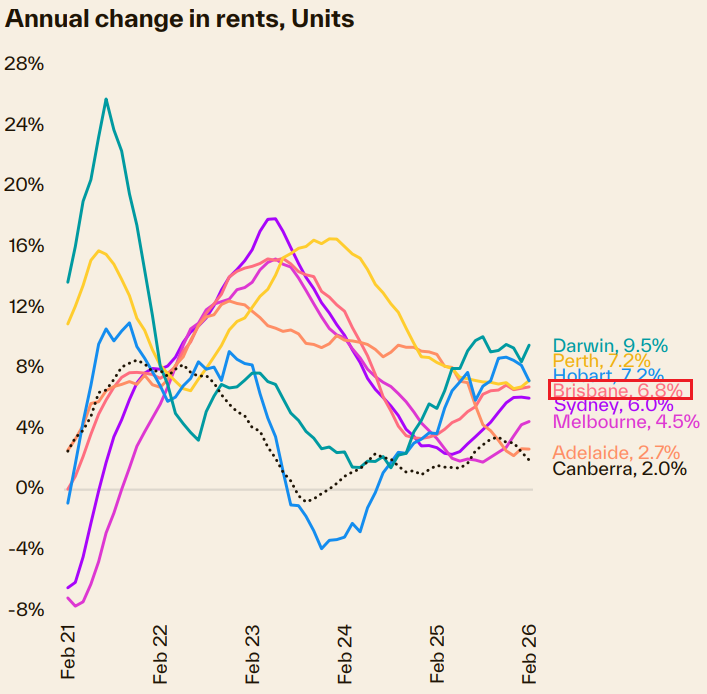

Brisbane’s Rental Market

Brisbane’s rental market remains firmly under pressure. The vacancy rate in Greater Brisbane was recorded at 1.0% in January, well below the 3% level typically associated with a balanced market. Annual house rent growth stands at 6.3%, unchanged from January, whilst unit rent growth of 6.8% is also steady, both continuing to outpace inflation and compound affordability challenges for renters.

Gross yields remain stable at 3.2% for houses and 4.0% for units, both unchanged from last month. Despite yields sitting below long-run averages, investor appetite has not diminished. Investors currently comprise 41.1% of housing finance commitments in Queensland, compared with a decade average of approximately 33%. This elevated participation reflects continued confidence in Brisbane’s rental fundamentals and ongoing return prospects.

Nationally, the rental index rose 0.7% in February, the strongest monthly result since October 2024. Building approvals data suggests that new housing supply will remain insufficient to address the shortage in the foreseeable future. Whilst approvals have lifted modestly from recent lows, construction lag times of twelve to twenty-four months mean that meaningful new supply will not reach the market until at least 2027. For renters and prospective buyers alike, there is little relief on the supply side in the near term, which continues to underpin both price and rent growth across Brisbane.

Source: Cotality |

Source: Cotality |

Summary

February has delivered another month of broad, data-supported growth across Brisbane’s property market. Values rose across all dwelling types, annual growth rates accelerated, and the structural conditions underpinning performance, constrained supply, tight vacancy, and sustained buyer demand, remain firmly in place.

Three headwinds warrant monitoring. First, the escalating geopolitical instability in the Gulf region, where military confrontations involving the United States, Israel and Iran have produced widespread airspace closures, flight disruptions through Dubai and Doha, and risks to global shipping. Events of this nature can weigh on consumer confidence, and any flow-through to Australian property sentiment deserves close attention in the weeks ahead.

Second, political uncertainty surrounding potential reforms to negative gearing and capital gains tax concessions ahead of the May 2026 Federal Budget. Whilst nothing has been legislated, Treasury is understood to be actively modelling options. Uncertainty of this kind has historically been sufficient to pause investor decision-making, and given investors comprise 41.1% of Queensland’s housing finance commitments, any sustained hesitation from this cohort could ease competitive pressure in segments most reliant on investment demand.

Third, the February RBA cash rate increase to 3.85%, with further hikes remaining possible, will erode purchasing power and may dampen near-term confidence.

However it is our view that these headwinds are unlikely to reverse Brisbane’s underlying trajectory.

Supply remains deeply constrained, vacancy is tight, and incomes are rising. The Home Guarantee Scheme continues to underpin first-home buyer activity. The fundamental imbalance between housing supply and demand in Brisbane continues to favour a market where values will, over time, move higher – even if the path is not entirely linear. The buyers and investors who succeed in this environment will be those who remain disciplined, understand the nuance of individual suburbs and property types, and act with conviction when the right asset presents itself.

We hope that you have found our Brisbane Property Market Update February 2026 helpful.

Connect with us today

To book a FREE discovery call ~ Click Here