By Melinda Jennison | April 2026

Introduction

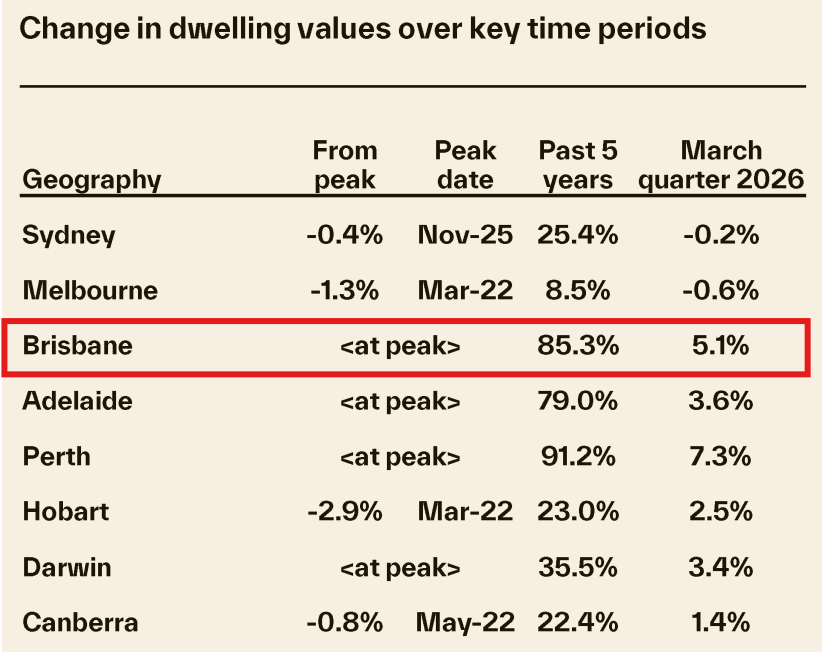

March 2026 has reinforced Brisbane’s position as one of Australia’s strongest-performing property markets, even as the operating environment has grown more complex. According to Cotality’s Home Value Index to 31 March 2026, Brisbane dwelling values rose 1.8% for the month, 0.2 percentage points above February’s 1.6% result, with the annual gain accelerating to 19.0% from 17.3%. The median dwelling value now sits at $1,101,151, up from $1,080,538 a month prior, and Brisbane dwelling values have risen 85.3% over the past five years.

Source: Cotality

The Reserve Bank of Australia followed its February rate rise with a further 25 basis point increase in March, lifting the cash rate to 4.10%, just 25 basis points below the recent cycle high. The RBA’s decision reflected inflationary pressures that have built significantly through the second half of 2025, with the Board signalling that inflation is expected to remain above target for some time and that risks are skewed toward higher inflation for longer. Adding to the difficult backdrop, the ANZ-Roy Morgan Weekly Consumer Confidence Index fell to its lowest reading on record in March, a level not seen since the series commenced in 1973, driven by anxiety over the Middle East conflict, rising energy costs, and the prospect of further rate increases.

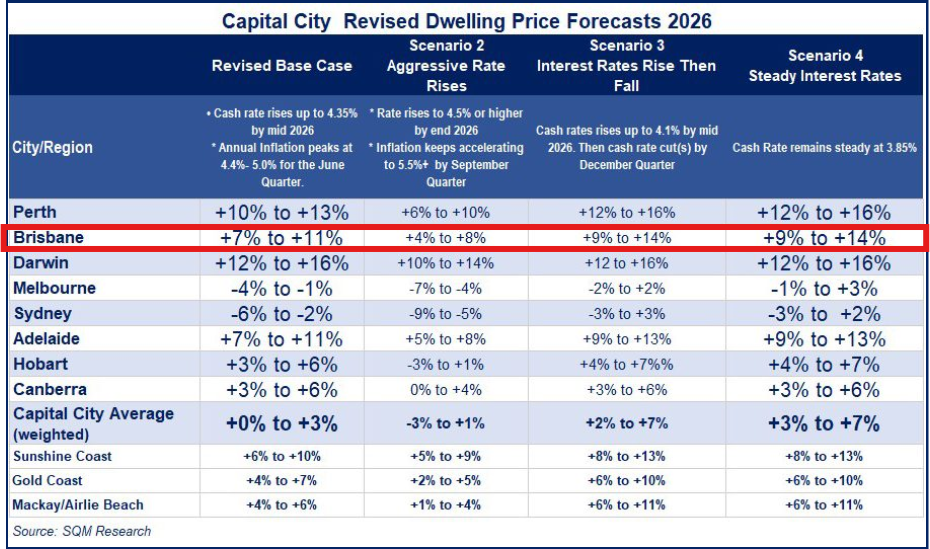

These pressures have prompted SQM Research to revise its 2026 national housing forecasts sharply downward. Under its revised base case, weighted capital city price growth is forecast at just 0% to +3% for the year, down from the prior projection of +6% to +10%. In contrast to this, Brisbane is still expected to outperform the national average rising between +7% and +11%, which is a downgrade from +10% to +15% as previously forecasted.

Source: SQM Research

Key drivers of the revision include energy price pass-through, limited wage growth amid AI-driven changes to labour demand, and broader affordability erosion. Potential government energy rebates may provide some offset, though SQM does not expect them to fully revive momentum. Perth, Darwin, Adelaide and Brisbane retain the strongest individual outlooks, whilst Sydney (forecast -6% to -2%) and Melbourne (-4% to -1%) face the sharpest headwinds from forecasted constraints.

According to Cotality data, auction clearance rates eased to an average of 65.55% throughout March, down from February’s 70.4%, though still higher than the same time last year. This softer result reflects a more cautious buyer mindset in response to rising interest rates, international uncertainty, higher living costs, and proposed policy changes around negative gearing and capital gains tax for property investors. From what our team observed at Brisbane auctions over the month, several properties that passed in still attracted multiple registered bidders. The issue was that bidding did not reach vendors’ price expectations, pointing to a widening gap between buyers and sellers rather than a lack of genuine interest. Private treaty remains Queensland’s dominant sales method, and passed-in properties frequently proceed to sell under that process.

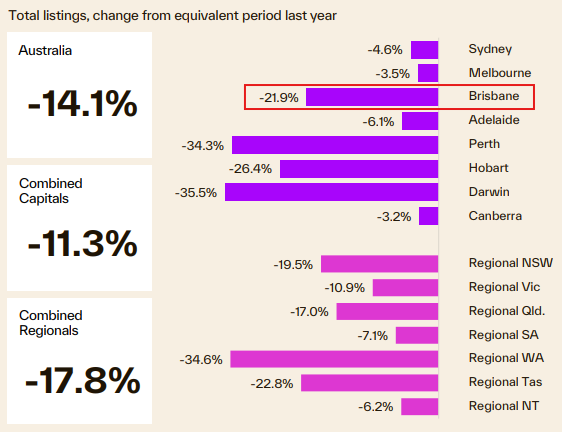

Listing volumes across Brisbane remain close to historic lows, with total advertised stock approximately 21.9% below year-ago levels, a stark contrast to Sydney and Melbourne, where volumes are more aligned with long-term averages. This structural undersupply, in place since 2020, continues to sustain competition for quality properties across Brisbane. Investors account for 40.1% of Queensland finance commitments, whilst first home buyers – buoyed by October 2025 incentives – represent 27.3% of commitments, up from 25.3% in February, driving strong demand in the sub-$1 million bracket.

Source: Cotality

Brisbane Dwelling Values

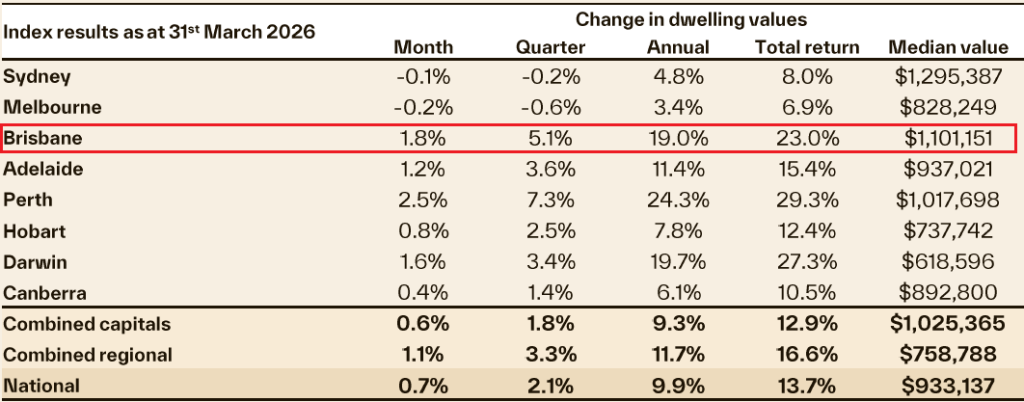

Brisbane’s median dwelling value of $1,101,151 at end of March represents monthly growth of 1.8%, quarterly growth of 5.1% and annual growth of 19.0%. These are all improvements on February’s respective figures of 1.6%, 4.8% and 17.3%. PropTrack’s independent Home Price Index confirmed positive monthly growth of 0.7% for Brisbane in March, consistent with the Cotality trend.

Source: Cotality

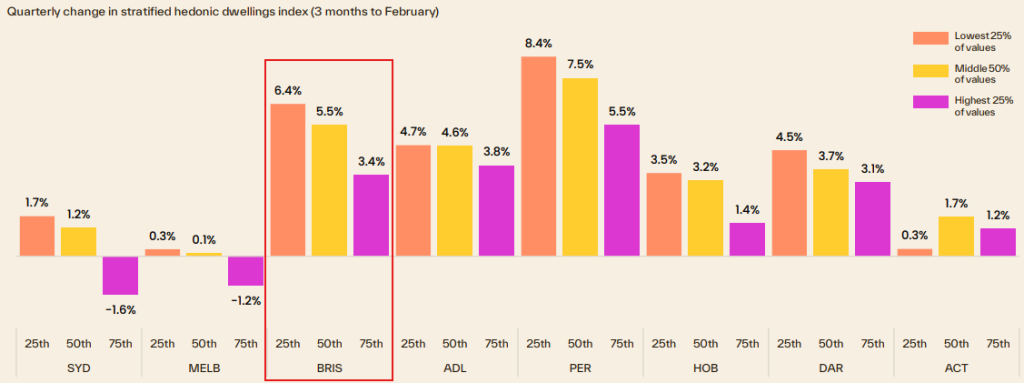

Cotality’s stratified index for the three months to February 2026 shows Brisbane’s lower quartile dwellings rose 6.4%, the middle 50% gained 5.5%, and the top quartile grew 3.4%. This is a slight easing in the upper segment compared with the prior quarter’s 4.0%, whilst the bottom and middle of the market have held firm. This pattern reflects serviceability constraints continuing to direct buyer demand toward more affordable price points, a trend reinforced by first home buyer activity below the $1 million mark across Brisbane.

Source: Cotality

Brisbane House Values

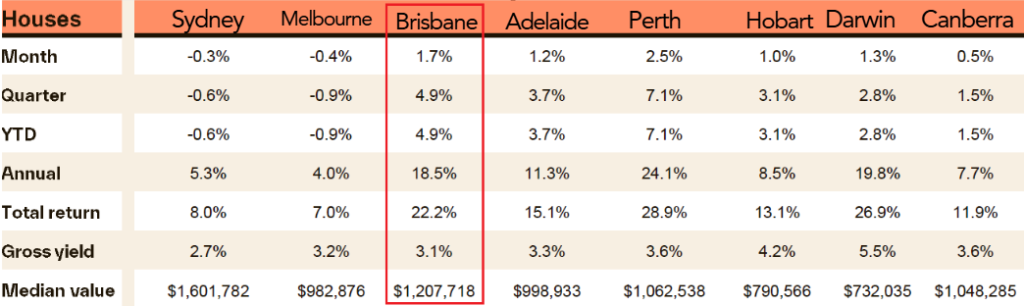

The median house value in Greater Brisbane rose to $1,207,718 in March, from $1,175,981 in February. Monthly growth of 1.7% is 0.2 percentage points above February’s 1.5%. The quarterly gain improved to 4.9% from 4.6%, and annual growth of 18.5% accelerated from 16.7% the month prior, placing Brisbane second only to Perth nationally.

PropTrack reported house price growth of 0.6% for March, suggesting a reacceleration from the prior month.

Source: Cotality

Brisbane Unit Values

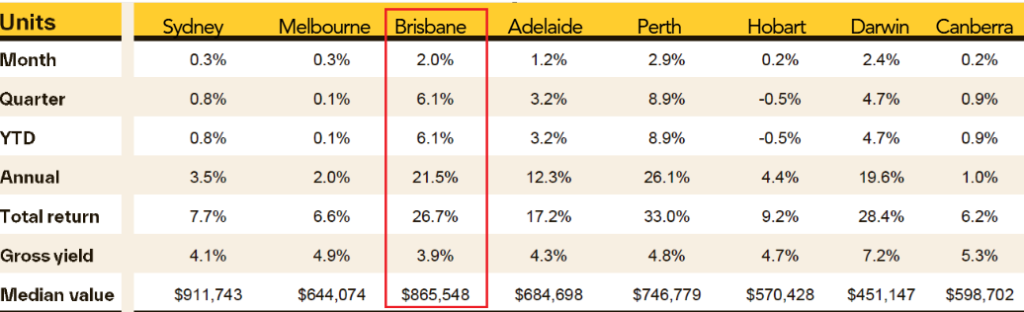

Brisbane’s unit market remains one of the strongest performers nationally. The median unit value reached $865,548 in March, up from $844,844 in February, with monthly growth of 2.0%. This reflects a marginal easing of 0.1 percentage points from February’s 2.1%. The quarterly gain of 6.1% improved from 6.0%, and annual growth of 21.5% accelerated from 20.1%, placing Brisbane second only to Perth amongst the capitals.

PropTrack confirmed unit price growth of 0.7% for March.

Source: Cotality

Brisbane’s Rental Market

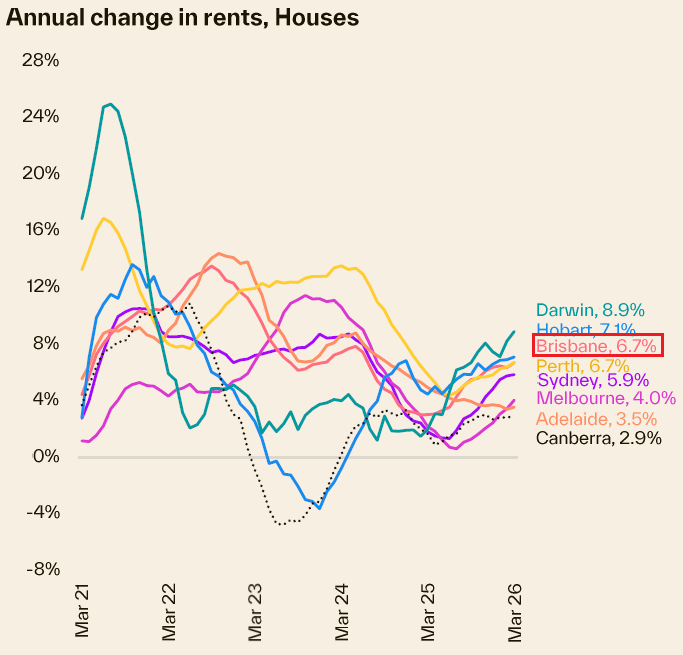

Brisbane’s rental market remains under pressure. The vacancy rate for Greater Brisbane was recorded at 0.9% in February, well below the threshold associated with a balanced market, and one of the tightest readings of any capital city nationally.

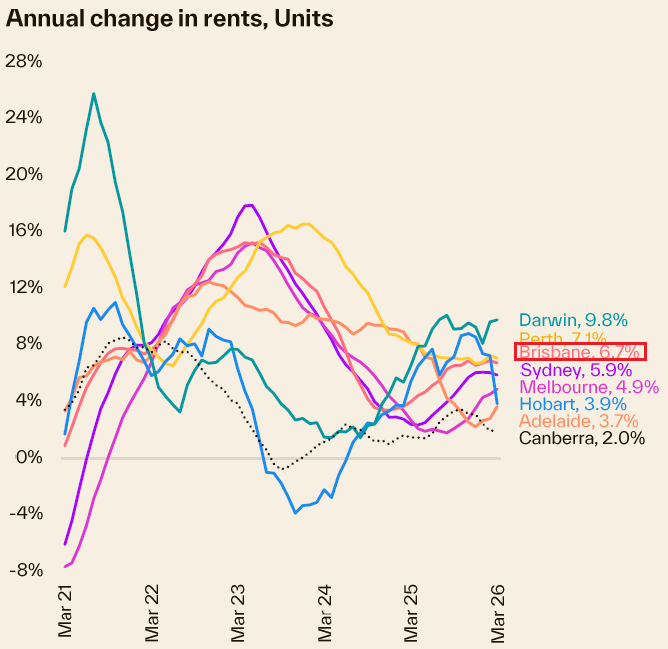

Annual house rent growth accelerated to 6.7% in March, up from 6.3% in February, whilst annual unit rent growth of 6.7% represents a slight easing from 6.8% the prior month. Both measures continue to outpace inflation, compounding affordability challenges for renters.

Gross rental yields have compressed slightly as capital value growth outpaces rent increases. Houses are currently returning 3.1% gross, down from 3.2% in February, and units are yielding 3.9%, down from 4.0%. Nationally, gross rental yields have been gradually declining since 2023 and Brisbane is following the same trajectory. The ongoing reacceleration in market rents is also relevant to the inflation outlook. Rents carry a 6.6% weighting in the CPI, and CPI rental inflation historically follows market rents with approximately a twelve-month lag, which may add further upward pressure on inflation in the period ahead.

Source: Cotality |

Source: Cotality |

Summary

March 2026 has delivered another month of strong headline data from Brisbane, yet the market is entering a clearly more complex phase. Rising interest rates, record-low consumer confidence, international instability, and political uncertainty around negative gearing and capital gains tax reform represent genuine headwinds. These factors are dampening sentiment and are likely to moderate the pace of price growth in the months ahead.

However, the fundamental drivers of Brisbane’s market remain intact. Supply is chronically constrained, with listings nearly 22% below year-ago levels. Rental vacancy sits at just 0.9%. There are still more buyers than sellers, which is the primary reason Brisbane continues to record growth whilst Sydney and Melbourne have turned negative. Unlike Brisbane, Sydney and Melbourne are seeing listing volumes that are more in line with long-term averages, which is contributing to the divergence in market conditions.

Buyers are expected to remain cautious through Easter and into autumn as consumer confidence stays under pressure. That said, unless listing volumes increase meaningfully, demand appears sufficient to maintain upward pressure on values, particularly for quality homes and investment-grade properties, though the magnitude of monthly gains is expected to ease from the strong pace recorded early in 2026. A sharp correction is unlikely given Brisbane’s structural undersupply. The pace of growth may slow, but the foundations supporting Brisbane property values remain firmly in place as we enter the second quarter of 2026.

We hope that you have found our Brisbane Property Market Update March 2026 helpful.

Connect with us today

To book a FREE discovery call ~ Click Here

Follow us on LinkedIn | YouTube | Instagram | TikTok

Read the Brisbane Property Market Update February 2026