The Federal Budget 2026 has created a lot of noise for property investors. With the proposed changes to negative gearing and capital gains tax, it is easy to see why some investors may now assume the “smart” move is to pivot immediately towards brand-new property.

That may include off-the-plan apartments, newly completed apartments, townhouse projects or greenfield house-and-land packages. After all, the policy settings are clearly designed to steer investor demand towards new housing supply.

But tax incentives should never be confused with investment fundamentals.

At Streamline Property Buyers, our concern is that many investors will be encouraged to make knee-jerk decisions based on tax treatment, rather than focusing on the quality of the underlying asset. And history has shown us, time and again, that buying property for tax benefits alone is rarely the best strategy for building long-term wealth.

What has changed?

Under the Federal Budget announcements, negative gearing will be limited to new builds from 1 July 2027. Existing arrangements remain unchanged for properties held before Budget night. For established residential investment properties purchased after 7:30pm AEST on 12 May 2026, investors will still be able to negatively gear up until 1 July 2027, but after that point, losses will no longer be deductible against other income such as wages. Instead, those losses will be quarantined and carried forward so they can be offset against future residential property income, including the ability to offset against future capital gains.

Capital gains tax is also changing. From 1 July 2027, the Government proposes to replace the 50 per cent CGT discount with cost base indexation and introduce a 30 per cent minimum tax on capital gains. Importantly, the CGT reforms will only apply to gains arising after 1 July 2027, and investors in new builds will be able to choose between the existing 50 per cent CGT discount and the new arrangements.

On the surface, this creates a clear incentive to buy new.

But that does not mean brand-new property is automatically a better investment.

Tax benefits do not create investment-grade property

A quality investment asset should be assessed on its long-term fundamentals. These include location, scarcity, land value, owner-occupier appeal, local income levels, infrastructure, walkability, school zones, employment access, rental demand and the likelihood of future capital growth.

Brand-new property often looks attractive on paper because it can offer depreciation benefits, lower immediate maintenance costs and, under the proposed new rules, more favourable tax treatment. But investors must ask a much deeper question:

Will this asset still be highly desirable in 10, 20 or 30 years’ time?

Many new properties, particularly off-the-plan apartments and greenfield house-and-land packages, have a high proportion of their value tied up in the building itself. Buildings depreciate. Land appreciates when it is scarce, well located and in demand.

That is why established properties in tightly held, land-constrained locations often outperform generic new stock over the long term. The tax treatment may be less attractive from a cash flow perspective, but the underlying asset may have stronger capital growth prospects.

And it is capital growth, not tax deductions, that usually creates meaningful long-term wealth.

The Government also benefits from new property

It is important to understand that when investors are steered towards brand-new property, governments also benefit.

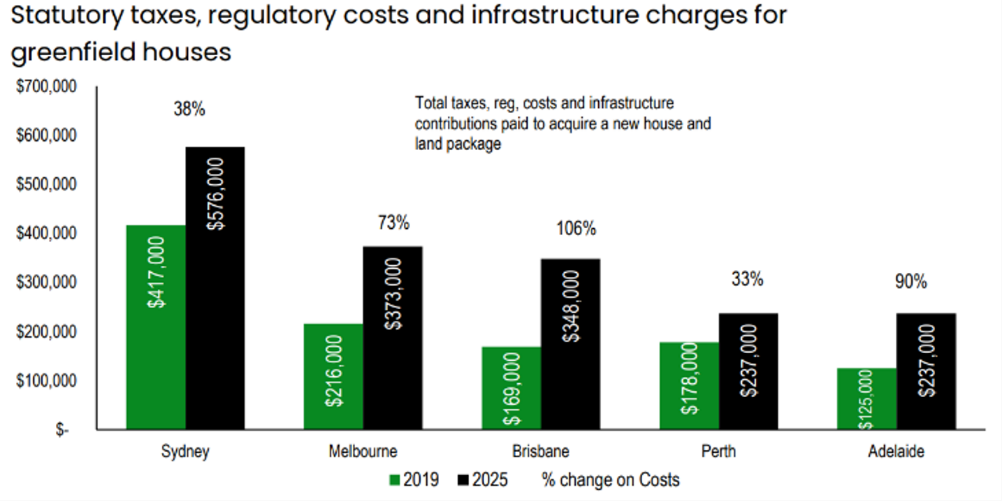

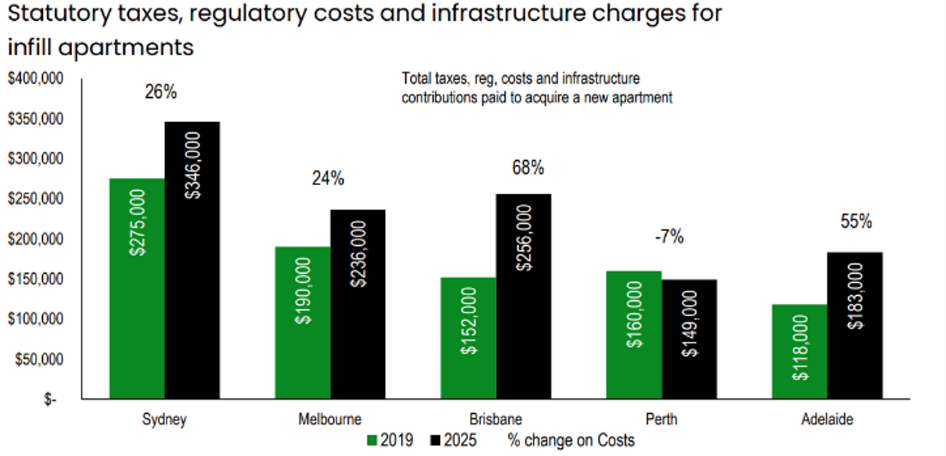

New housing carries significant layers of tax, statutory charges and regulatory costs. These can include GST, stamp duty, infrastructure charges, land tax during development, payroll tax through the construction supply chain, council-related costs and compliance costs. These costs are ultimately built into the price paid by the end buyer.

Research commissioned by the Housing Industry Association and prepared by the Centre for International Economics has previously estimated that government taxes, regulatory costs and charges can represent a very significant share of the cost of new housing. For example, HIA reported that Brisbane buyers face taxes and charges of up to $348,000 on greenfield homes and approximately $256,000 on infill apartments, with substantial proportions also identified in other capital cities.

Source HIA |

Source HIA |

The point is not that new property is always bad. Australia desperately needs more housing supply.

The point is that investors should understand what they are paying for. A brand-new property price often includes a lot more than the land and dwelling. It may also include developer margin, marketing costs, sales commissions, GST and a range of government-imposed costs.

That can create a premium on day one.

Artificial demand can distort the market

Another concern is that these Budget changes may artificially increase demand for brand-new property.

First-home buyers have long been encouraged into the new-build segment through grants, concessions and other government incentives. Now investors may be pushed into the same segment because of negative gearing and CGT treatment.

That means two groups – first-home buyers and investors – may be competing for the same product type, not necessarily because it is the best asset, but because policy settings have directed them there.

This can inflate demand and pricing in the new-build market. But an investor should be very careful about relying on policy-driven demand as a growth strategy.

The real test comes at resale.

A brand-new property does not remain brand new forever. Once it is sold into the secondary market, it generally becomes established property. The next buyer may not receive the same tax advantages that applied to the original purchaser. This can reduce the depth of the resale market, particularly if the property is in an area dominated by investors or where there is an ongoing pipeline of newer competing stock.

That is a very real risk.

Investor concentration creates another layer of risk

When a large volume of investors is drawn into the same type of property in the same location, additional risks emerge.

High investor concentration can lead to multiple similar properties being available for rent at the same time. This can increase vacancy risk and put downward pressure on rents, particularly in new apartment precincts, townhouse corridors or greenfield estates where many properties settle around the same period.

It can also create resale risk. If many investors decide to sell at the same time, or if future buyers prefer newer stock in nearby stages of development, the resale market can become thin.

This is one of the biggest risks with generic new-build stock. There may be very little scarcity.

If there are hundreds of similar apartments, townhouses or house-and-land packages nearby, an investor has limited control over their competitive position. The property may need to compete on price, rent, inclusions or incentives. That is very different from owning a scarce, well-located asset in an established suburb where replacement supply is limited.

The negative gearing changes may not affect all investors equally

The Government’s messaging has focused heavily on fairness and helping first-home buyers. But one practical reality is often missing from the discussion.

Higher-income investors may still be able to absorb weaker annual cash flow. They may also be more likely to seek professional advice around ownership structures, tax planning and portfolio strategy.

The quarantining of losses is also important. While investors may no longer be able to claim losses annually against their PAYG income for affected established properties, those losses are not necessarily lost forever. They can be carried forward and used against future residential property income, including capital gains.

This means some investors may still decide that a high-quality established asset is worth holding, even if the annual cash flow is less attractive.

In other words, the policy may not stop sophisticated investors from buying quality assets. It may simply make it harder for less experienced, less wealthy mum and dad investors to understand their options.

The negative gearing changes may not affect all investors equally

The biggest mistake investors can make right now is to start with the tax benefit and work backwards.

A better approach is to start with the asset.

- Is the property scarce?

- Is the location desirable?

- Is there strong owner-occupier demand?

- Is the land component meaningful?

- Is future supply constrained?

- Is the rental demand deep and diverse?

- Will the property appeal to buyers in the resale market without relying on tax incentives? And even more importantly…

- What is your long term goal as an investor?

Only after those questions have been answered should tax treatment and cash flow be considered.

Tax matters. Cash flow also needs to be considered. But neither should override asset selection.

Seek advice before making a knee-jerk decision

We expect to see a wave of marketing from developers, project marketers and off-the-plan sales groups promoting new property as the obvious solution to the Budget changes. In fact, this messaging has already started appearing in investor inboxes.

Investors need to be very careful.

The best property investment decisions are made with a long-term lens. What looks attractive immediately after a policy announcement may not produce the best outcome over a 20- or 30-year investment horizon.

At Streamline Property Buyers, our team includes Qualified Property Investment Advisers who understand property markets through practical experience, not just theory. We know that policy changes can influence short-term behaviour, but long-term performance still comes back to fundamentals.

The Budget may change the tax landscape. It does not change the principles of quality asset selection.

For investors, the message is simple. Do not buy brand-new property purely because the tax treatment looks better. Understand the full cost, the resale risk, the supply pipeline, the tenant profile and the long-term growth prospects.

Because when it comes to building wealth through property, the right asset will always matter more than the tax deduction.

Connect with us today

To book a FREE discovery call ~ Click Here

Follow us on LinkedIn | YouTube | Instagram | TikTok

Tune into our podcast ~ Brisbane Property Podcast