Why The Headlines Are Only Part Of The Story

At a recent live event at Ballymore Stadium, I joined Daniel Anderson, Scott Lumsden and Barry Wilkinson for a panel discussion on Brisbane property, tax policy and the market signals that matter most beyond Brisbane property news. The room was full of questions, and for good reason. Many buyers and investors are seeing strong headlines suggesting that property prices may fall sharply. Auction clearance rates have softened, buyer sentiment has shifted quickly, and the Federal Budget announcements have caused many investors to pause while they reassess their strategy, cash flow and borrowing capacity.

That caution is understandable. A property purchase is a large financial decision, and when the rules around tax treatment change, buyers need time to understand how those changes may affect their position. Some investors are reviewing whether established property still fits their plan. Others are considering whether a new build may suit their circumstances. Many are waiting for more certainty before committing.

But caution is not the same as collapse. One of the key themes from the panel was that national commentary often treats Australia as a single market, when the data tells a far more local story. Sydney and Melbourne carry significant weight in national numbers because of their size and transaction volumes. When those markets slow, national headlines can look far worse than the conditions being experienced in Brisbane.

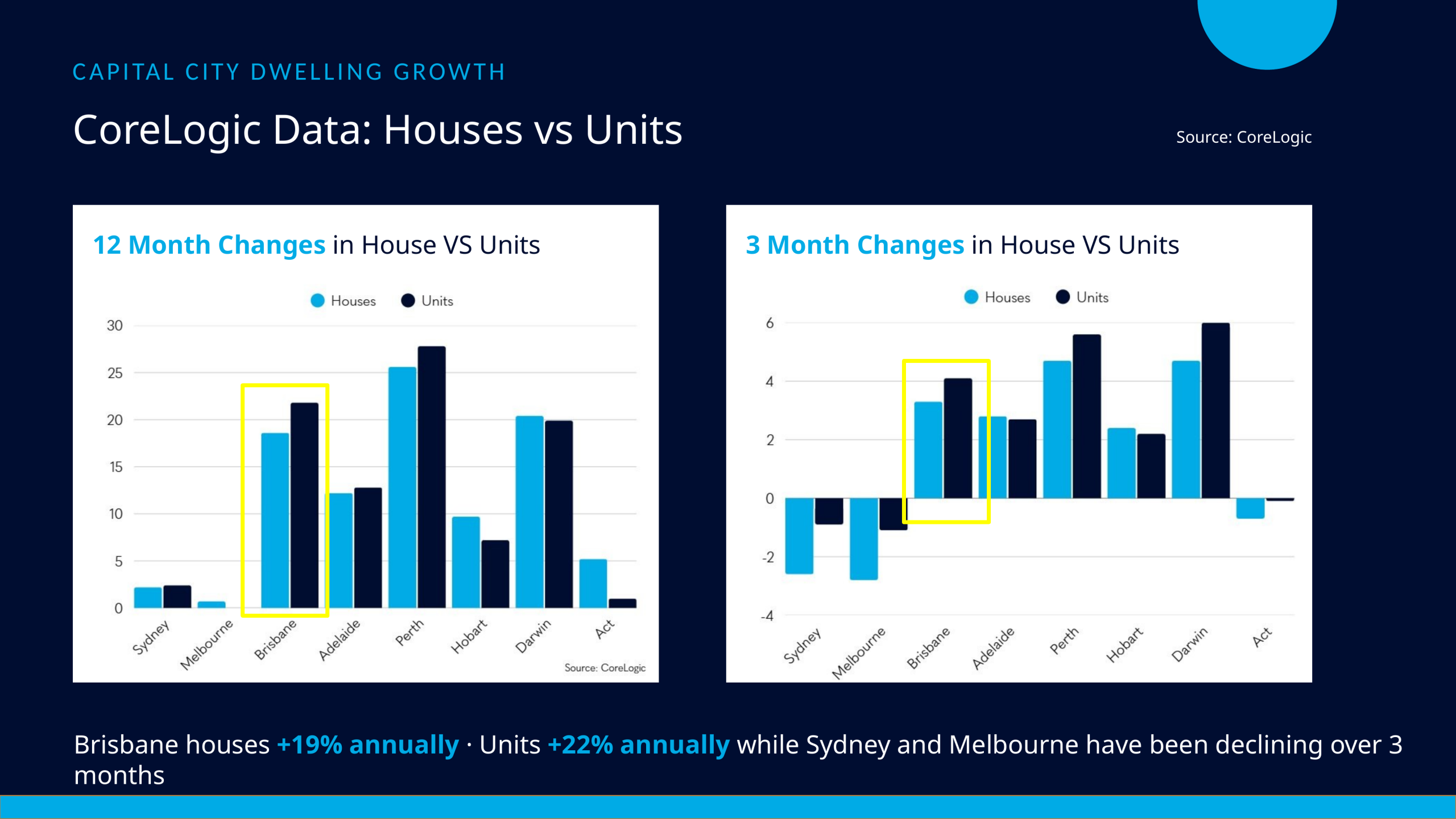

The Brisbane data remains strong. CoreLogic figures presented on the night showed Brisbane houses were up 19 per cent annually, while Brisbane units were up 22 per cent annually. On a three-month view, Brisbane remained one of the top three capital city markets for growth across both houses and units. By comparison, Sydney and Melbourne had recorded negative growth over the quarter.

Figure 1: CoreLogic capital city dwelling growth – houses versus units.

That does not mean buyer behaviour has not changed. On the ground, we are seeing more nervousness, longer decision-making timeframes and less urgency. After the very strong price appreciation Brisbane has experienced since COVID, this moderation is not necessarily a bad thing. A calmer market can help buyers take a more measured approach. What matters is separating short-term sentiment from the underlying drivers of long-term value.

The Brisbane Fundamentals That Still Matter

The main reason we remain confident in Brisbane is that the market is still supported by four core fundamentals: tight housing supply, high construction costs, strong interstate and overseas migration, and the long-term economic impact of the 2032 Olympic and Paralympic Games, together with the infrastructure program attached to that event.

Figure 2: Key demand drivers supporting Brisbane property.

Tax policy can influence demand. It can change buyer preferences. It can alter cash flow calculations and affect borrowing capacity. But tax policy cannot quickly create more homes, reduce construction costs, or remove the need to house a growing population. This is where Brisbane’s story differs from some of the larger capital city markets.

Supply: More Listings, But Still Not Enough

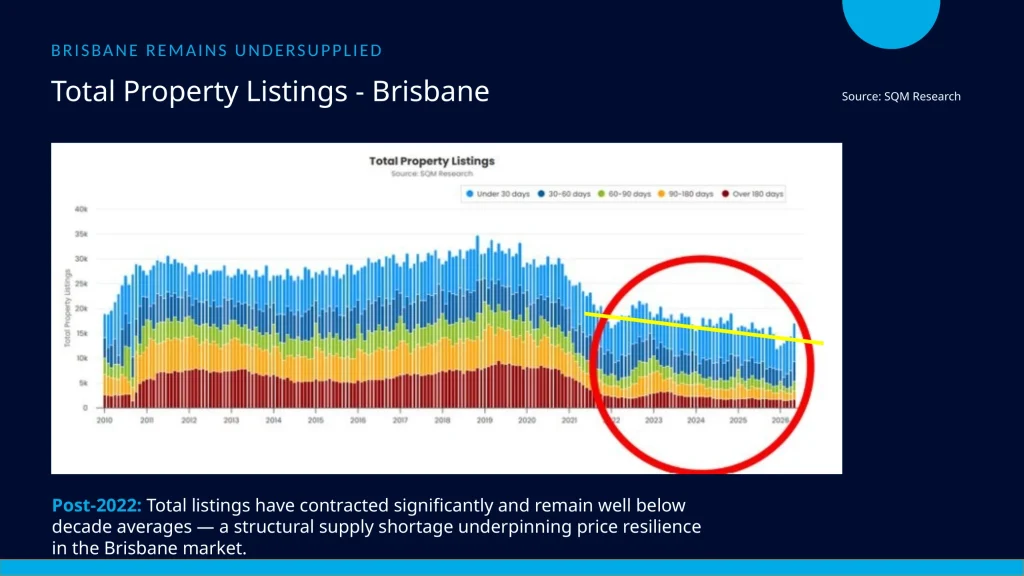

Supply is the first piece of the puzzle. SQM Research data presented at the event showed total property listings in Brisbane have contracted significantly since 2022 and remain well below long-term averages. Historically, Brisbane has often sat somewhere around 28,000 to 32,000 total listings. More recently, listings have remained below 20,000 for an extended period. Yes, listings have increased month-on-month over recent months, but we are still well short of what would be considered a balanced level of available stock.

That context is critical. A market can record an increase in listings and still be undersupplied. This is exactly what we are seeing in Brisbane. More choice may ease some of the intense competition buyers have faced, but it does not automatically mean the market is oversupplied.

Figure 3: Brisbane total property listings remain well below long-term averages.

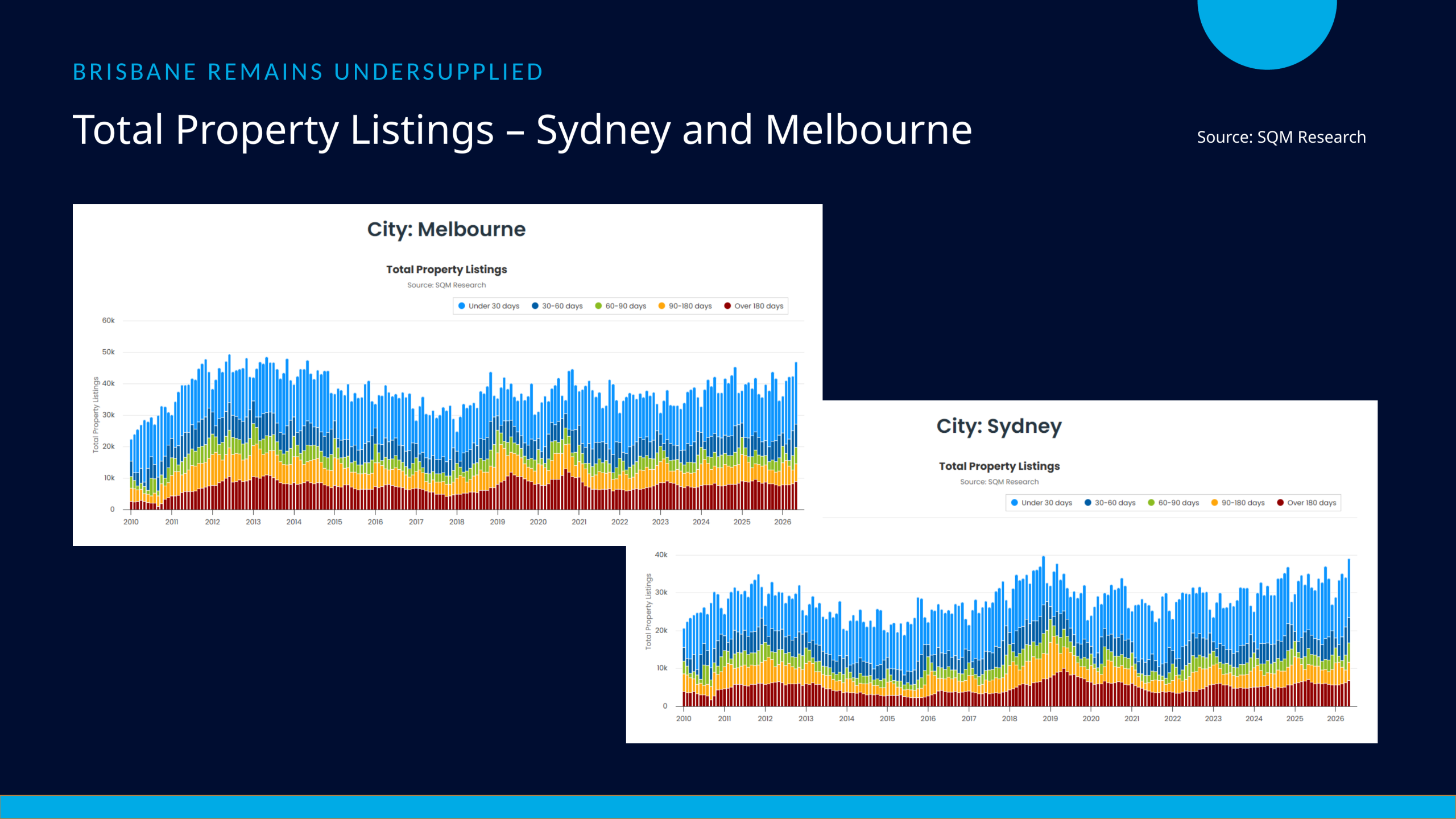

When we compare Brisbane with Sydney and Melbourne, the difference becomes clearer. The SQM Research charts for Sydney and Melbourne show listing volumes sitting much closer to their long-term trends. Those markets have different supply conditions, different affordability constraints and different recent growth patterns. This is why broad national statements about property prices need to be tested against local data before buyers rely on them.

Figure 4: Sydney and Melbourne listing trends show different supply conditions.

Why New Supply Remains Hard to Deliver

The second supply challenge is what we are building, not just what is currently listed for sale. Altus Group forecasts show Brisbane construction costs are expected to be 90.3 per cent higher than 2019 levels by 2028. That is a larger increase than Perth at 74.3 per cent, Sydney at 64.6 per cent and Melbourne at 60.5 per cent.

This matters because it directly affects the feasibility of delivering new dwellings. South East Queensland already faces pressure from labour shortages, material costs and a major infrastructure pipeline. As the region prepares for 2032, those pressures are unlikely to disappear. Higher construction costs make it harder to bring affordable new supply to market, which keeps pressure on the existing housing base.

Figure 5: Altus Group construction cost forecasts by capital city.

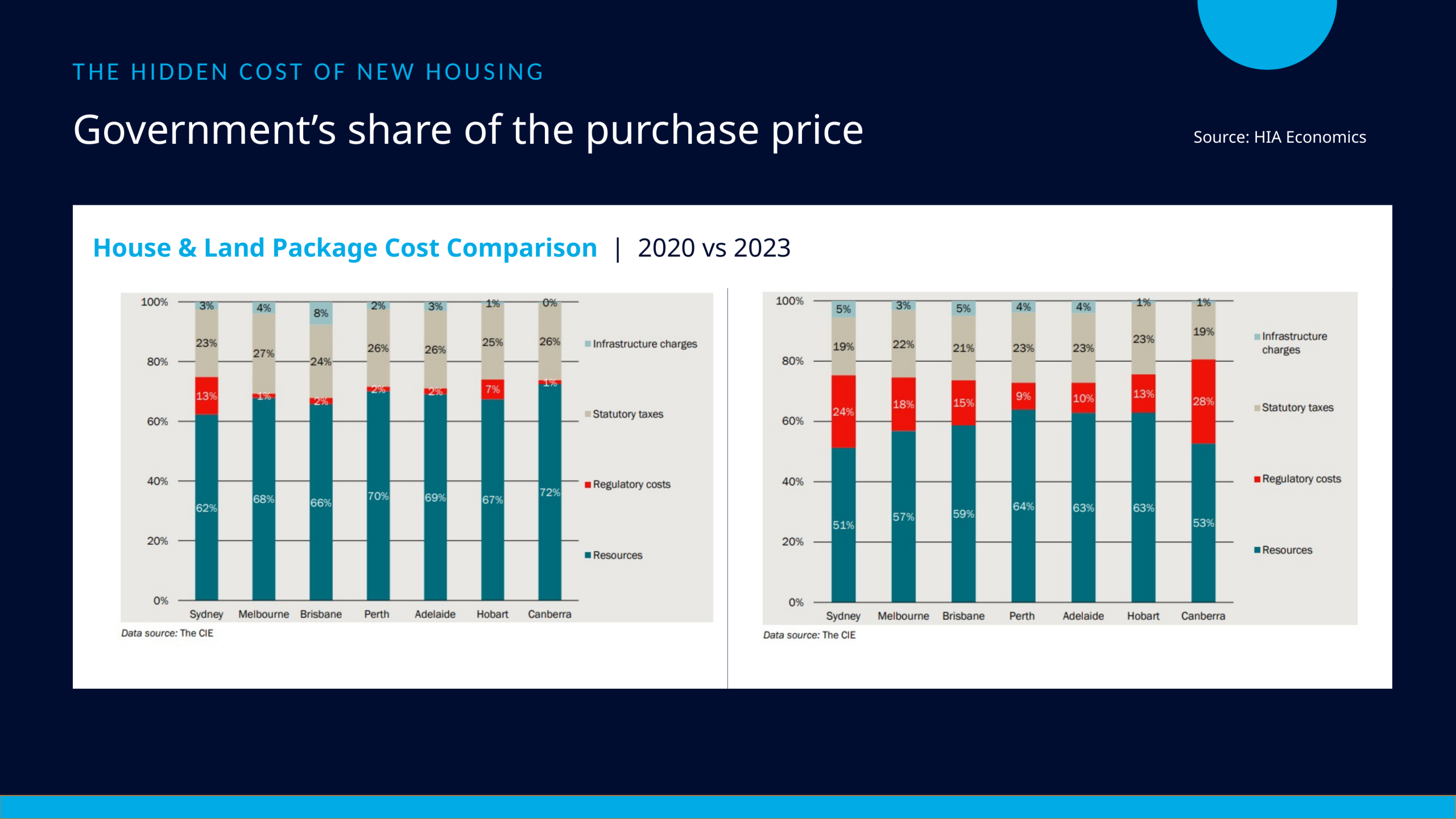

This is also why pivoting to brand new property should not be treated as a broad-based recommendation for every investor. New property can be the right fit in some circumstances, but it must be assessed carefully. HIA Economics data on the hidden cost of new housing shows that in Brisbane, a smaller share of the purchase price is going towards the resources that deliver the dwelling itself, with a meaningful proportion absorbed by regulatory costs, statutory taxes and infrastructure charges.

For house and land packages, the Brisbane chart showed resources accounted for 66 per cent in 2020, with the balance made up of these additional costs. By 2023, resources accounted for 59 per cent, while the combined government-related share had risen to 41 per cent. For attached dwellings in Brisbane, the 2023 figures also showed 59 per cent in resources and 41 per cent in the additional charges. These costs are not always obvious to buyers, but they have a real effect on feasibility, affordability and long-term investment performance.

Figure 6: HIA Economics – the hidden cost of new housing in Brisbane.

Demand Continues to Outpace Delivery

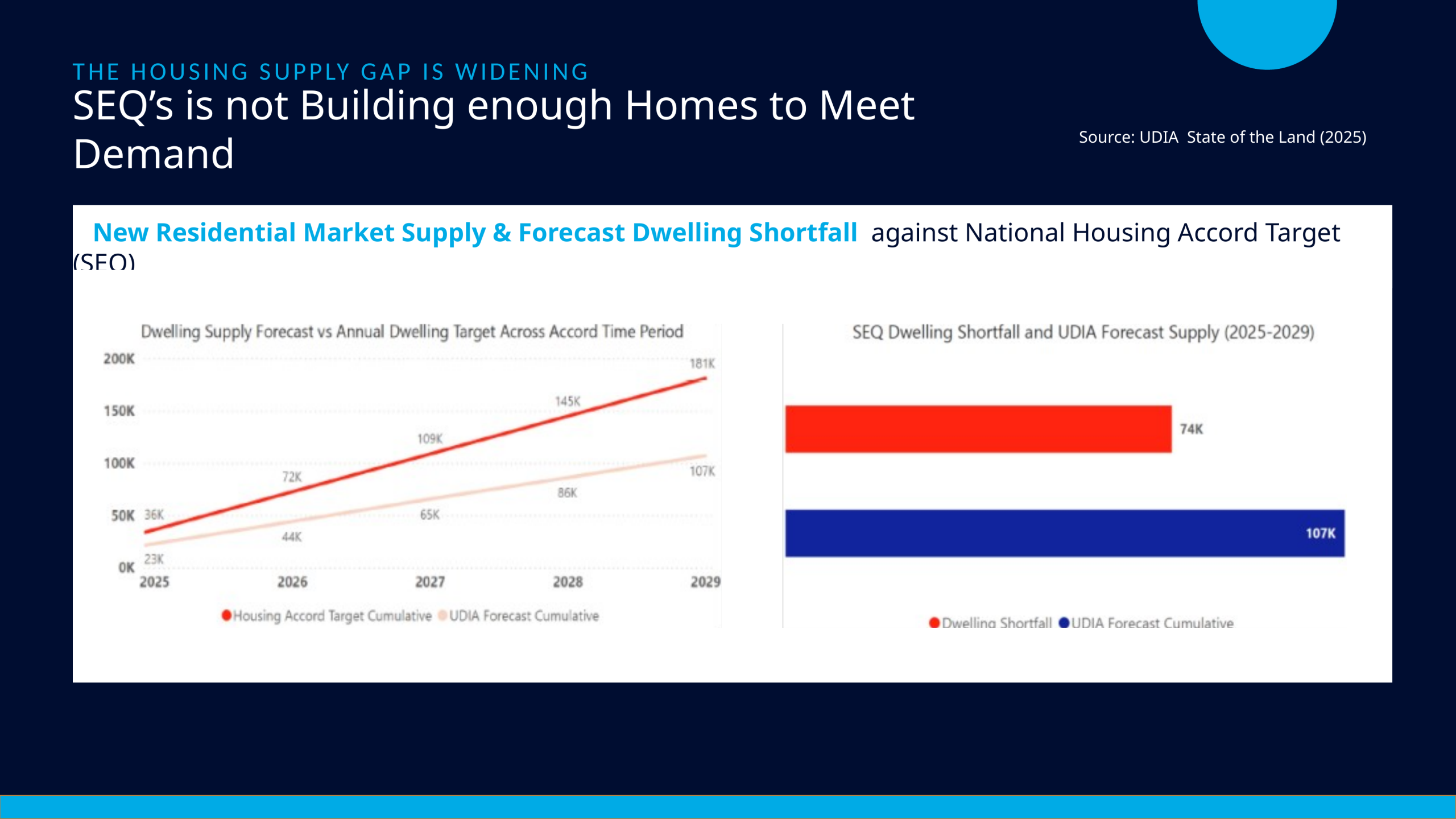

The supply gap becomes even clearer when we look at the National Housing Accord targets for South East Queensland. UDIA State of the Land data presented on the night showed a widening shortfall between the homes the region needs and the homes forecast to be delivered. Across the 2025 to 2029 period, the cumulative target was shown at 181,000 dwellings, compared with a forecast supply of 107,000 dwellings, leaving a projected shortfall of 74,000 homes.

Figure 7: South East Queensland forecast dwelling shortfall against Housing Accord targets.

At the same time, demand continues to build. The ShapingSEQ regional plan projects South East Queensland’s population to grow from 3.78 million to 5.94 million by 2046, with growth of around 86,400 people per annum. Queensland continues to attract strong interstate migration, as well as a high level of net overseas migration. More people need somewhere to live, and that demand is arriving while listings remain low and new supply is constrained.

Figure 8: ShapingSEQ population forecasts and migration data.

The infrastructure story adds another layer. Brisbane and South East Queensland have a $107 billion infrastructure pipeline across 2023/24 to 2027/28. Major projects include the Brisbane Olympic Stadium at Victoria Park, the National Aquatic Centre at Spring Hill, Cross River Rail, Logan–Gold Coast Faster Rail, The Wave Rail, the Coomera Connector and Queen’s Wharf. These projects support jobs, economic activity and long-term connectivity. They also bring more workers into a region that is already stretched for housing.

Figure 9: Brisbane 2032 and the major infrastructure pipeline.

What Buyers Should Do Now

So, will tax policy changes affect the market? Yes. We are already seeing a shift in sentiment, and some investors are reassessing their plans. Certain property types and locations may experience weaker demand if the numbers no longer stack up. Buyers should never ignore policy settings, cash flow or borrowing capacity.

But the bigger point is this: tax policy does not change the fundamentals for Brisbane.

The opportunity in Brisbane is still real, but it is not a reason to buy anything, anywhere, at any price. For buyers and investors, this is a moment that calls for clear thinking and qualified, independent advice. Understanding where the genuine opportunities lie, which property types and locations are best positioned given the evolving policy environment, and how to structure a purchase for long-term success are more important questions than ever. Buyers need to understand the difference between national headlines and local evidence. They need to know which locations are supported by owner-occupier demand, where infrastructure is meaningful, where supply remains constrained, and which assets have the best chance of holding value through changing policy cycles.

The strategy of buying the right property in the right location and holding for the long term has not changed. But navigating the current environment well requires expertise, and that is precisely when professional guidance matters most. For those who are prepared, informed and well advised, Brisbane remains a market with strong long-term support. The headlines may be loud, but the fundamentals are still doing the heavy lifting.

If you would like to discuss how Brisbane’s market fundamentals apply to your own property goals, we welcome the conversation.

Connect with us today

To book a FREE discovery call ~ Click Here

Follow us on LinkedIn | YouTube | Instagram | TikTok

Tune into our podcast ~ Brisbane Property Podcast